ICHRA vs. Group Health Insurance: Which Is Right for Your Business?

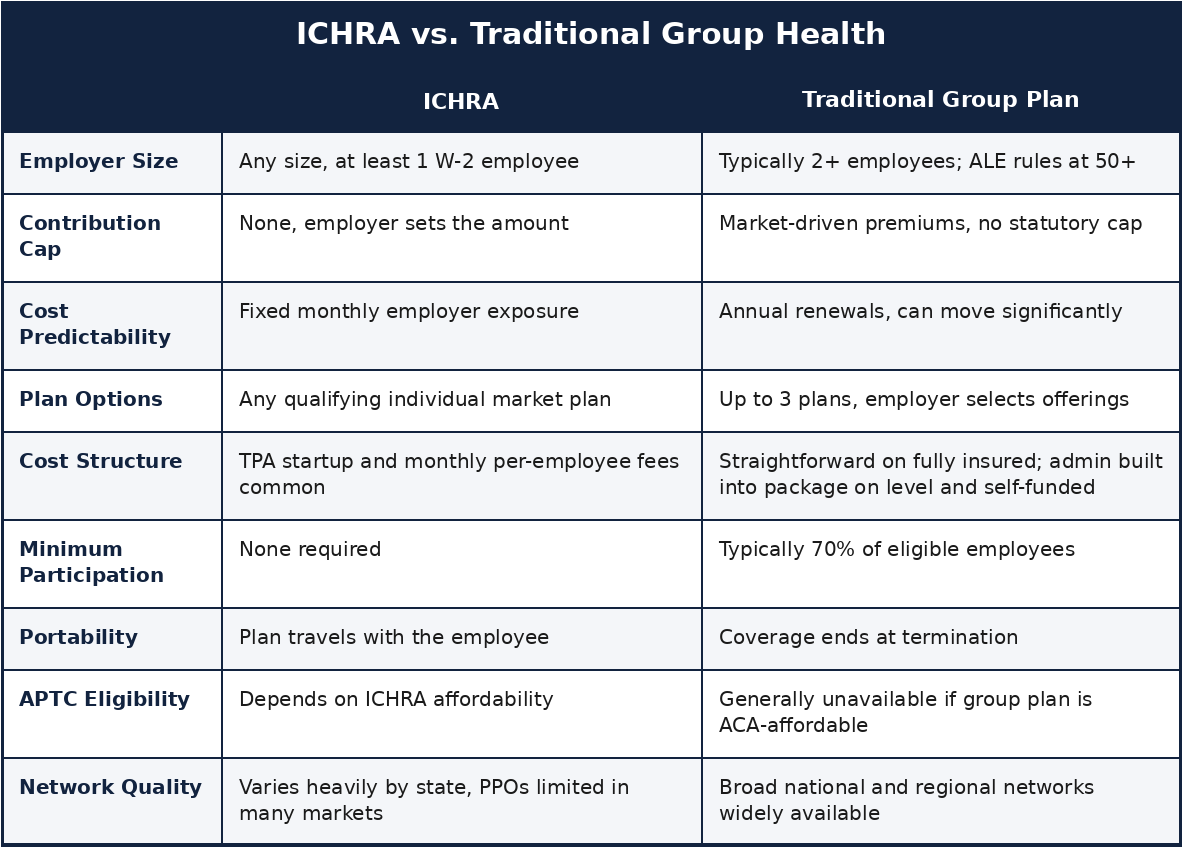

An Individual Coverage Health Reimbursement Arrangement (ICHRA) is an employer funded, tax advantaged account that lets businesses of any size reimburse employees for individual health insurance premiums and qualifying medical expenses, instead of offering traditional group health insurance. The employer sets a monthly allowance, the employee buys their own individual coverage, and the reimbursement comes back tax free on both sides, income tax free to the employee, payroll tax free to the employer.

ICHRA came out of final rules issued June 20, 2019 by the IRS, Treasury, the Department of Labor, and HHS, effective for plan years starting on or after January 1, 2020. Before that, HRAs had to be integrated with a group plan. The 2019 rules dropped that requirement and created ICHRA as its own standalone benefit category for the first time. Unlike the Qualified Small Employer HRA, which only works for employers under 50 full time employees, ICHRA is open to any employer size and carries no statutory contribution cap.

If you’re weighing employer health insurance options for the first time, or wondering whether commercial health insurance through a group plan still makes sense for your business, this breaks down both options.

How It Works

The employer sets a maximum monthly allowance per employee, and that number can vary by employee class, age, and family size. The employee shops for any qualifying individual plan, ACA Marketplace on or off exchange, Medicare if applicable, or other individual market coverage, and submits monthly proof of coverage and expenses. The employer reimburses, tax free, on both sides.

An employee offered an ICHRA can’t also be eligible for the employer’s group plan, though an employer can offer group coverage to one class of employees and an ICHRA to a different class. The rules define 11 permitted employee classes, full time, part time, salaried, hourly, seasonal, geographic, union, and others, so there’s real structure available when designing benefits across a mixed workforce. Within a class, benefits have to be offered on equal terms, though age based variation (up to 3:1 between oldest and youngest) and family size adjustments are both allowed.

One structural difference gets glossed over constantly: under ICHRA, the employee is the one paying the bill. They pay their individual insurer directly, submit proof, and get reimbursed. If an employee misses a payment and their individual plan lapses, that’s not something the employer can just fix administratively the way you’d handle a payroll deduction hiccup on a group plan. Missing a premium payment and losing individual coverage does not qualify as a life event that opens up a new enrollment window. Once that plan is terminated for non-payment, the employee is locked out of the individual market until the next Open Enrollment period, and unless they have an unrelated qualifying life event in the meantime, that wait can run months.

A note on timing: Open Enrollment dates vary by state and can shift from year to year due to federal or state legislative changes, so employers and employees should confirm current deadlines directly with their state’s marketplace, or with a licensed broker, before relying on any specific date. For 2027, most marketplaces will run November 1 through December 15, with a couple of state specific exceptions: Pennie starts earlier, on October 15, and New Jersey’s window runs through December 31. What doesn’t change is the underlying risk: whichever window applies, once it closes, a lapsed individual plan generally can’t be reinstated without a qualifying life event. Check your specific marketplace for updated Open Enrollment dates before making any decisions.

ICHRA does come with its own 60 day Special Enrollment Period, and it is not strictly a one-time thing, it recurs each year tied to the plan’s renewal date, not just the initial eligibility date. But for the common calendar-year ICHRA, that renewal window falls at the same time as standard Open Enrollment anyway, so it doesn’t actually help someone who lapses mid-year, outside that window. It only provides real extra runway for employers running an ICHRA on an off-calendar plan year, where the renewal SEP lands at a different point in the year than standard Open Enrollment. Either way, that’s a real gap in coverage, and a real administrative risk, that a group plan simply doesn’t carry.

Where the Group Market Holds Its Own

The group market is not in any kind of decline, and we want to say that plainly before getting into ICHRA mechanics, because a lot of ICHRA content skips straight past it. Group stays profitable for carriers, which keeps it competitive: most carriers let small groups offer up to three plans at once, as long as each plan has at least one enrolled employee, so a one size fits all benefit was never the only option on the group side to begin with. Fully insured rates are straightforward and predictable for the plan year. Level funded and self funded arrangements carry admin costs built into a negotiated package, but those costs are transparent and known upfront, not tacked on separately after the fact.

Where ICHRA differs is in the administration. Most ICHRA arrangements run through a third party administrator, and many TPAs charge startup fees plus monthly per employee admin charges on top of whatever the employer is already contributing, a genuine cost difference worth weighing before assuming ICHRA is automatically the cheaper option.

The Individual Market Reality

This is the part most ICHRA materials skip entirely, and it matters enormously depending on where your employees actually live. We service roughly 18 states, and in most of them there is no PPO available on the individual market at any price point an employer or employee would consider reasonable. What’s actually available is largely EPO and HMO coverage with narrow, state bound networks.

Carrier participation is shrinking as well, and not just at the edges. CVS Health’s Aetna exited the ACA individual exchanges after the 2025 plan year, affecting roughly 1 million members across 17 states. Cigna has announced it will exit entirely after 2026, affecting another 369,000 members across 11 states. CareSource is exiting West Virginia, Ohio, and Indiana after 2026, leaving roughly 60,000 people in Indiana and 28,000 more in Ohio to find new coverage, on top of Kentucky, Michigan, and North Carolina, which it already exited a year earlier. Baylor Scott & White Health Plan is leaving the Texas marketplace after 2026 as well, affecting about 100,000 enrollees there, roughly 2.6% of the entire state marketplace.

That’s four carriers, and they’re not the only ones. As of mid-2026, at least nine insurers have announced full or partial ACA marketplace exits for 2027, including PacificSource, Providence Health Plan, and Mending (formerly Taro Health), each pulling out of individual states or regions. Between the roughly 1 million already displaced by Aetna’s exit and the well over half a million more set to be displaced by Cigna, CareSource, and Baylor Scott & White this coming Open Enrollment, that’s well over a million and a half people nationally affected within about two enrollment cycles, and Texas is taking a direct hit from two of the upcoming exits at once. That leaves only UnitedHealthcare and Anthem from the top 5 health insurance carriers (UnitedHealthcare, Anthem, Cigna, Aetna, and Humana) with meaningful national presence in the individual market. Fewer carriers competing for the same business tends to push rates in one direction, and the trend lines for 2027 already point higher.

We recently consulted with a couple in New Jersey, both in their 60s. Their COBRA option was a Gold EPO plan with a $2,000 deductible, and that COBRA premium was less than the cheapest Bronze plan available to them on the individual market in New Jersey, a state with no PPOs on the individual ACA market whatsoever. The only carrier with anything resembling national access there is Ambetter, and it isn’t even available in every county. When we priced out a Gold level individual plan comparable to their COBRA coverage, premiums ran north of $4,000 a month, climbing as high as $6,000 a month for a plan that only offered limited Pennsylvania access. COBRA, with the better deductible, ended up cheaper.

That’s the individual market a meaningful share of ICHRA eligible employees are actually shopping in. An ICHRA allowance that looks generous on paper doesn’t change the underlying network and carrier limitations in a given state.

Where It Actually Fits

None of this means ICHRA is the wrong tool. It means it’s the right tool in specific circumstances, not a universal replacement for group health insurance. It tends to work best for employers under 50 employees, mainly because those employers carry no ACA mandate to offer coverage in the first place, so there’s no compliance floor to clear. It also works best for employees who aren’t already subsidy eligible, since ICHRA dollars go furthest for people who wouldn’t otherwise be pulling an APTC.

It fits naturally when a workforce is spread across multiple states and a single group plan simply can’t serve everyone well, or when the employer happens to sit in a state where the individual market still has real carrier participation and competitive pricing, which, as the New Jersey example shows, is not something to assume. For small or solo operations where group coverage isn’t available or isn’t affordable in the first place, ICHRA can be the only workable option, provided the local individual market actually has something worth buying.

Not sure which one actually fits your business? That’s what we’re here for. We shop fully insured, self funded, level funded, ICHRA, and non ICHRA options side by side, and depending on your employees’ income levels, a marketplace subsidy may genuinely be the better route than anything an employer can offer directly. We run the real numbers against your specific state, workforce, and budget before recommending anything. Book a free consultation for an in-depth customized analysis catered to your business.

This is also where ICHRA can backfire for lower and moderate income employees. If an employee would otherwise qualify for an Advance Premium Tax Credit (APTC), every dollar of employer ICHRA contribution reduces that subsidy by roughly the same amount. If the ICHRA is deemed affordable for that employee, they lose APTC eligibility entirely. If it’s deemed unaffordable, they keep APTC eligibility, but the credit still gets calculated net of the employer contribution, so the employer’s money largely just substitutes for subsidy dollars the employee would have gotten anyway. Add a TPA fee on top of that, and an employer can end up spending real money to produce little or no net improvement for that employee. ICHRA tends to make the most sense for employees who weren’t subsidy eligible to begin with.

Outside of an ICHRA, the only real way an employer can help with individual coverage is grossing up an employee’s pay, which adds taxable income and simply hopes the employee applies it to premiums and handles the Marketplace paperwork correctly on their own. That gross up also gets hit with FICA on both sides, adding cost beyond the dollar amount itself. ICHRA avoids both problems: the contribution is tax free to the employee and payroll tax free to the employer, and it’s structurally tied to coverage rather than just extra cash in a paycheck.

ACA Compliance for Larger Employers

For Applicable Large Employers (50 or more full time equivalent employees), an ICHRA has to meet the ACA affordability standard to satisfy Employer Shared Responsibility under Section 4980H. An ICHRA is affordable when the employer’s monthly contribution exceeds the Lowest Cost Silver Plan premium minus the affordability percentage multiplied by the employee’s household income. That percentage moves every year: 8.39% for 2024, 9.02% for 2025, and 9.96% for 2026. Three IRS safe harbors (W-2 wages, rate of pay, and federal poverty line) let you run affordability calculations without needing each employee’s exact household income.

Employers also have to provide written notice at least 90 days before the ICHRA plan year begins, covering the allowance amount, start date, dependent coverage, how it interacts with premium tax credits, and the 60 day Special Enrollment Period the employee is entitled to. That SEP also means an ICHRA can launch at any point during the year, not just January 1.

Philadelphia-Area Considerations

Independence Blue Cross, at the time of writing, currently allows a one person small group plan as long as that single employee isn’t a family member of the business owner. A company with one unrelated W-2 employee can qualify for small group coverage under IBX, and IBX small group rates have historically priced more competitively than equivalent individual market coverage in this region. Where that holds true, the financial case for switching to an ICHRA weakens considerably, and it’s a market specific dynamic that national level ICHRA content consistently misses.

Do It For Me Insurance

We work across the full range of business health benefits, group health insurance, level and self funded arrangements, and ICHRA where it genuinely applies, and we run the real numbers for your specific market before recommending anything. Whether you’re comparing employer health insurance options for the first time or reevaluating your commercial health insurance strategy, we are here to help.

Ready to find out which option actually saves your business money? Book your free consultation and we’ll run the numbers for your workforce before you decide anything.

Frequently Asked Questions

Is ICHRA cheaper than group health insurance? Not automatically. Group rates are predictable and TPA fees on ICHRA arrangements add real cost. Whether ICHRA saves money depends on your workforce size, location, and how many employees would otherwise qualify for ACA subsidies.

Can a small business offer both group health insurance and ICHRA? Yes, but not to the same employees. An employer can offer group coverage to one class of employees and an ICHRA to a different class, as long as the classes follow the 11 permitted categories under the rule.

Does ICHRA affect an employee’s ACA subsidy? It can. If the ICHRA is deemed affordable, the employee loses APTC eligibility entirely. If it’s deemed unaffordable, they keep eligibility, but the subsidy is calculated net of the employer’s contribution.

What size business can offer an ICHRA?

Any size. Unlike the Qualified Small Employer HRA, which is limited to employers with fewer than 50 full time equivalent employees, ICHRA has no employer size limit and no statutory contribution cap.

Sources

- IRS, Health Reimbursement Arrangements (HRAs) — ICHRA final rule background

- Federal Register, Health Reimbursement Arrangements and Other Account-Based Group Health Plans — June 20, 2019 final rule

- Mercer, 2026 affordability percentage for employer health coverage increases — 2024/2025/2026 ACA affordability percentages

- STAT News, Cigna to exit ACA individual market in 2027 — April 30, 2026

- Healthcare Dive, Cigna exits ACA exchanges despite dramatic profit growth in Q1 — confirms Aetna/CVS exit after 2025

- Healthinsurance.org, Health insurers are exiting the Marketplace again — CareSource and Baylor Scott & White exit details and member counts

- Becker’s Payer Issues, 9 insurers exiting ACA markets — full list of 2027 carrier exits

- KFF, Tracking Insurer Participation Changes in the ACA Marketplaces in 2027 — national context on the exit wave

- Healthinsurance.org, An SEP if you’re offered a QSEHRA or ICHRA — confirms the ICHRA SEP recurs at annual renewal, not just initial eligibility

- Healthinsurance.org, Premium Payments and Grace Periods — confirms non-payment does not trigger a Special Enrollment Period

- Independence Blue Cross, Small business plans — IBX small group eligibility (2 to 50 employees); one person group detail based on our direct broker experience with IBX underwriting